This is not just a smartphone story. It's a story about How success becomes a trap. How execution excellence becomes a prison that prevents innovation. And how organizations, once they're trapped, rarely escape.

Indian Smartphone Case

A little over a decade ago, Indian smartphone brands were unstoppable. Walk into any electronics store in 2013-2015, and you'd see Micromax, Karbonn, Lava, Intex, Spice and Xolo everywhere. The shelves were theirs. The customers were theirs. The momentum was absolutely theirs. And the numbers were impressive.

In 2015, Indian smartphone brands-controlled more than 40% of the Indian market. Micromax alone shipped 7.5 million units that year. For a brief moment in 2014, Micromax overtook Samsung to become India's #1 smartphone brand by market share and got featured in world’s Top10 mobile brands.

Let that sink in for a moment: An Indian company, beating Samsung in its own backyard.

Fast forward to 2026, Indian smartphone brands are barely visible. Micromax has less than 1% market share. Karbonn, Lava, Intex, Spice - these names that once dominated retail shelves are now footnotes. Some are completely gone. The Indian market is now entirely controlled by Xiaomi, Vivo, Oppo, Samsung, Realme, and Apple.

A category that Indian companies once led is now overwhelmingly foreign-owned.

What happened in ten years?

Most people point to obvious suspects: Chinese competition, supply chain advantages, manufacturing scale, capital access, aggressive pricing. All true.

But there's a deeper story here.

It's a story about execution versus innovation. And it's a story that Indian auto brands need to read very carefully.

How Indian Smartphone Brands Won

The success of Indian smartphone brands wasn't luck. It was skill. Companies like Micromax, Karbonn, and Lava had something global competitors didn't: they understood the Indian market in their bones. They knew what a ₹10,000 smartphone buyer actually wanted (longer battery life, bigger screens, good cameras for the price). They understood retail in tier 2 and tier 3 cities. They had dealer relationships that went back years.

They built distribution networks that were envied. They trained retailers. They offered credit schemes that made phones affordable. They were incredibly good at one thing: selling and moving volumes.

The numbers show it. In 2013, Indian brands shipped 18.5 million units. By 2015, that number had grown to 38.6 million units, more than double in two years.

That's execution excellence.

But here's where the story gets interesting: execution excellence, on its own, is never enough.

Why Execution Becomes a Prison

This is a core insight from Management by Danda. When something is working, organizations naturally double down on what works. The sales team expands. Distribution improves. Pricing gets more aggressive. Volume increases. Quarterly targets get met. Everyone celebrates.

And the trap closes.

The organization becomes incredibly efficient at doing what it already knows. But it stops building what it doesn't know.

This is exactly what happened with Indian smartphone brands. They became elite execution machines. Their 6-month product cycles were fast. Their pricing decisions were smart. Their retailer relationships were deep. They could move 2 million phones in a quarter without breaking a sweat.

But while they were perfecting the present, someone else was building the future. Chinese manufacturers like Xiaomi, Oppo, and Vivo were doing something different. They were investing in things that take years to compound – design capabilities, product engineering teams, OS and software layers, camera technology and processing, battery management and manufacturing automation.

In 2013-2014, this investment wasn't visible. Xiaomi's phones didn't look radically different. The specs were similar. The price was comparable. But capability compounds. Slowly at first, then suddenly.

By 2017, Chinese phones had better cameras. By 2018, they had better software integration. By 2019, they offered better value. By 2020, they owned the market.

Indian brands, meanwhile, had perfected the art of selling phones that other companies designed.

Why Organizations Choose Execution Over Innovation

Here's the uncomfortable truth about organizations like most Indian smartphone companies.

The Danda system (fear-based management) loves predictability. It rewards:

- Measurable targets

- Visible quarterly results

- Guaranteed ROI

- Reduced risk

- Certainty

Innovation offers none of these.

When a sales manager asks for additional marketing budget, she can usually show expected returns: "If we spend ₹5 crores on advertising, we'll capture ₹100 crores in additional sales."

It's predictable. It's safe. It gets approved.

When an innovator asks for ₹5 crores to develop a new battery technology, the conversation is different:

CFO: "What is the ROI?"

Innovator: "We don't know yet. We're testing a hypothesis."

In a Danda system, that answer doesn't get budget.

So, innovation either gets starved of resources, or it gets packaged as "innovation theater," business cases with optimistic projections, financial models designed to justify investment, targets designed to look certain.

The organization becomes uncomfortable with uncertainty. Fear replaces curiosity. And when fear replaces curiosity in an organization, innovation slowly dies.

Indian smartphone companies didn't fail because they stopped trying hard. They failed because they became so busy executing the present that they forgot to build the future.

Indian Automotive Industry's Moment of Truth

The smartphone industry may be the most visible example of what happens when execution outpaces innovation. But it won't be the last.

The Indian automotive industry is standing at the exact same crossroads right now.

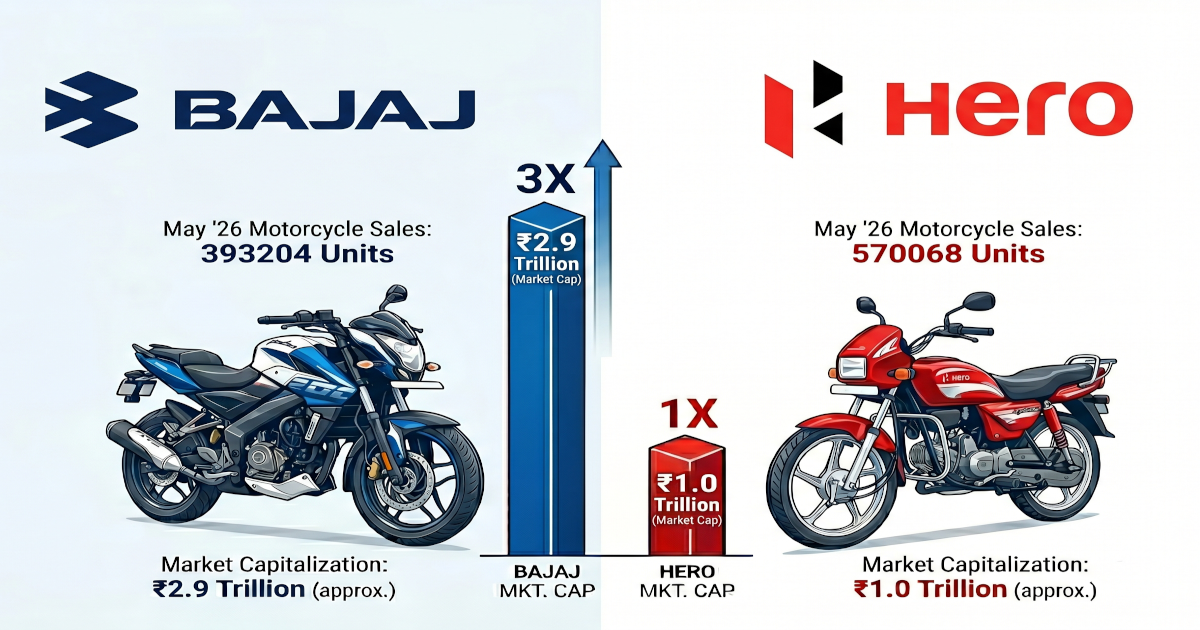

For decades, Indian manufacturers (Maruti, Hyundai, Tata, Mahindra, Hero Honda, Bajaj Auto) have built impressive strengths:

- Cost engineering (building cars for ₹5 lakhs that would cost ₹12 lakhs elsewhere)

- Manufacturing excellence (quality at scale)

- Localization (98% localization in component sourcing)

- Supplier development (creating entire supply ecosystems)

- Distribution and dealer networks

These capabilities have made India the world's 4th largest auto market and the 2nd largest two-wheeler market. Not bad. But the game is changing.

The future automobile is no longer just about engines and factories. It is being defined by Battery technology and EV platforms, Software and operating systems, AI and autonomous driving, Manufacturing innovation

This is where Chinese manufacturers have moved aggressively. BYD didn't start with decades of automotive experience. They started with battery expertise and built outward. Today, BYD is largest seller of EVs in world.

XPeng developed AI-powered autonomous driving features that are now competing with Tesla's Autopilot. Geely acquired Volvo and is now launching advanced EV platforms. NIO is creating premium EV experiences that challenge Mercedes and BMW.

Meanwhile, Indian automotive companies continue to enjoy: Strong domestic brands, Customer loyalty, Price advantage, Extensive distribution and more important Policy support.

These are real advantages. They provide time. But here's the lesson from smartphones: protection is not the same as competitiveness.

The Real Lesson

The decline of Indian smartphone brands wasn't primarily about technology or market share. It was about organizational priorities. One set of companies optimized for today's market. Another balanced today's execution with tomorrow's capabilities. One became expert at selling. The other became expert at building. One won market share. The other won the future.

This is the central lesson of Management by Danda.

Organizations rarely fail because they stop working hard. They fail because they become so busy executing the present that they stop building the future. And by the time the future arrives, someone else owns it.

Indian automobile manufacturers have distribution that Chinese companies are still trying to build. They have brands that customers trust. They have decades of manufacturing experience. They have policy support.

The question is not whether they can sell cars today.

The question is this: Are they investing enough to define mobility ten years from now?

Distribution can be replicated. Manufacturing can be learned. Cost advantages fade away. Technology leadership takes years to build, compound continuously, and becomes harder to catch up with, is something else entirely.

The smartphone industry learned this lesson the hard way. The question is: Will the automotive industry learn it before it's too late? Or will it become another chapter in the story of Indian execution excellence that forgot to build for tomorrow?